AI Generated Summary

- Yet when a key ally calls in a loan—part of which dates back to 1996-97—Pakistan cannot negotiate better terms or even secure a short extension without resorting to high-interest, short-term arrangements.

- Islamabad routinely burnishes its image as a nuclear-armed regional heavyweight, a linchpin in China’s Belt and Road Initiative via CPEC, and a valued partner to Gulf monarchies.

- The world sees not a confident power but a nation still trapped in the cycle it claims to….

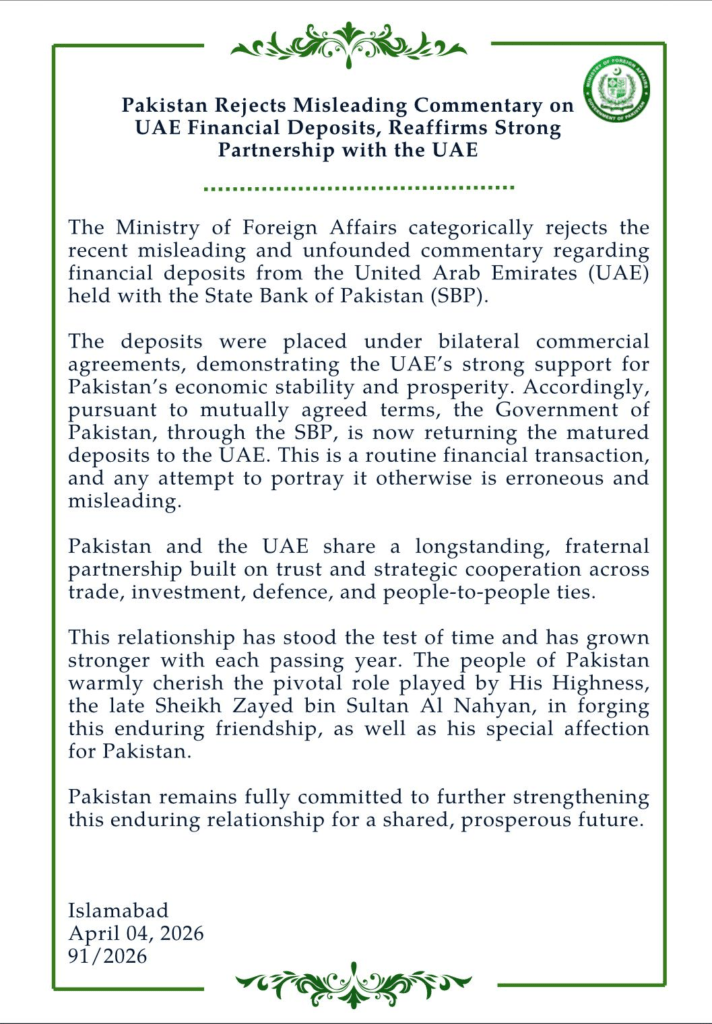

In a move framed as an act of sovereign pride, Pakistan has announced it will repay $3.5 billion in debt to the United Arab Emirates by the end of April 2026. A senior official described the decision as a price worth paying to uphold “national dignity,” insisting that financial considerations could not compromise it. Abu Dhabi had demanded the immediate return of funds originally extended in 2019 to stabilise Pakistan’s balance of payments. What was once routinely rolled over—recently on a precarious month-to-month basis—will now be returned in full, with phased payments reportedly including $450 million as early as next week, followed by $2 billion and $1 billion.

This is no minor accounting adjustment. Pakistan’s State Bank of Pakistan (SBP) holds roughly $16.38 billion in foreign exchange reserves as of late March. Repaying roughly $3 billion from these holdings would slash the central bank’s buffer by nearly 18 per cent, eroding import cover and external stability at a delicate moment. Total liquid reserves, including commercial banks, stand around $21.8 billion, yet the outflow coincides with other obligations: a $1.3 billion Eurobond matures on April 8, pushing April’s total repayments toward $4.8 billion. Analysts warn of renewed pressure on the rupee and complications for Pakistan’s ongoing $7 billion IMF Extended Fund Facility. Under the programme, Islamabad must secure about $12.5 billion in rollovers from China, Saudi Arabia and the UAE to meet external financing needs through September 2027. Losing UAE support without immediate replacement inflows is not a display of strength; it is a self-inflicted wound.

The official narrative of “dignity” rings hollow when examined against the facts. Pakistan had actively sought a two-year rollover and a reduction in interest rates from 6.5 per cent to around 3 per cent, citing improved credit ratings and lower global borrowing costs. The UAE refused. What Islamabad presents as a principled stand is, in reality, acquiescence to a creditor’s demand amid regional turbulence—the UAE’s own liquidity needs heightened by Middle East tensions following the US-Israel-Iran conflict. For decades, Gulf deposits have functioned as de facto lifelines; their abrupt withdrawal reveals how fragile that dependence remains.

This episode underscores a deeper contradiction in Pakistan’s foreign policy: a persistent desperation to project global standing while its economic reality tells a different story. Islamabad routinely burnishes its image as a nuclear-armed regional heavyweight, a linchpin in China’s Belt and Road Initiative via CPEC, and a valued partner to Gulf monarchies. Prime Minister Shehbaz Sharif’s government speaks of “brotherly” ties and strategic autonomy. Yet when a key ally calls in a loan—part of which dates back to 1996-97—Pakistan cannot negotiate better terms or even secure a short extension without resorting to high-interest, short-term arrangements. The rhetoric of dignity masks the beggar’s bowl. By rushing to repay, officials hope to reset the creditor-debtor dynamic and impress the IMF and markets. Instead, they risk signalling weakness: a country so cash-strapped it must liquidate reserves to avoid the optics of prolonged begging.

The setback is multidimensional. Reserves are not abstract numbers; they underpin import financing for fuel, food and machinery in an economy already grappling with inflation, low growth and structural deficits. A sharp drawdown could force tighter monetary policy or fresh borrowing on harsher terms, undermining the very stability the repayment ostensibly protects. It also strains relations with other Gulf partners who may now question Pakistan’s reliability as a steward of deposits. Far from enhancing global standing, this move advertises vulnerability. Pakistan’s leaders appear more concerned with performative sovereignty than sustainable sovereignty.

None of this is inevitable. Pakistan’s chronic reliance on external rollovers stems from decades of fiscal mismanagement, elite capture and failure to broaden the tax base or reform loss-making state enterprises. The IMF programme offers a roadmap, but cosmetic gestures like this repayment—however spun—cannot substitute for genuine reform. If “national dignity” means anything, it must begin with building an economy that does not lurch from rollover to repayment crisis.

Pakistan’s decision to return the UAE funds may salve short-term pride, but it delivers a long-term economic blow. The world sees not a confident power but a nation still trapped in the cycle it claims to have broken. Until Islamabad confronts this reality—rather than dressing it in the language of dignity—such setbacks will recur. True standing is earned through resilience, not through expensive displays of it.